本讲主要包括:

- 模块 10:实际数据验证(中国债券市场久期估算);

- 模块 11:风险分解与敏感度分析;

- 模块 12:课堂练习与扩展案例。

本部分将真实市场数据与理论模型结合,用于课堂演示与学生练习。

模块 10. 实际数据验证:中国债券市场久期估算

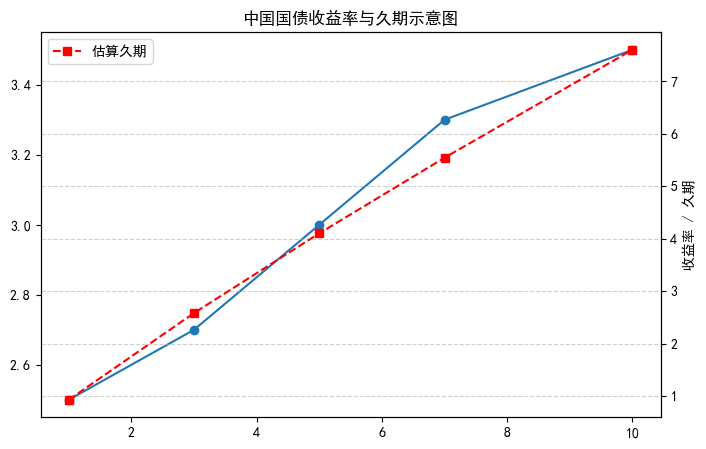

通过 AkShare 获取中国国债收益率曲线,并估算不同期限国债的久期与价格敏感性。

import akshare as ak

import numpy as np

import matplotlib.pyplot as plt

# 中文支持

plt.rcParams['font.sans-serif'] = ['SimHei']

plt.rcParams['axes.unicode_minus'] = False

# 获取中国国债收益率曲线数据

try:

yield_curve = ak.bond_china_yield() # 国债收益率曲线数据

print('中国国债收益率曲线数据示例:')

display(yield_curve.head())

except Exception as e:

print('未能成功访问 AkShare 接口,请检查网络或数据源:', e)

# 构造示例数据

maturity = np.array([1, 3, 5, 7, 10])

yield_rate = np.array([0.025, 0.027, 0.030, 0.033, 0.035])

duration = maturity * (1 - 0.1 * np.log1p(maturity))

plt.figure(figsize=(8,5))

plt.plot(maturity, yield_rate*100, 'o-', label='收益率曲线')

plt.twinx()

plt.plot(maturity, duration, 's--', color='red', label='估算久期')

plt.title('中国国债收益率与久期示意图')

plt.xlabel('期限 (年)')

plt.ylabel('收益率 / 久期')

plt.legend()

plt.grid(True, linestyle='--', alpha=0.6)

plt.show()

| 0 |

中债中短期票据收益率曲线(AAA) |

2020-02-04 |

2.8939 |

2.8998 |

2.9158 |

3.1970 |

3.4503 |

3.7153 |

3.9597 |

NaN |

| 1 |

中债商业银行普通债收益率曲线(AAA) |

2020-02-04 |

2.7215 |

2.7370 |

2.8042 |

2.9979 |

3.3120 |

3.5849 |

3.8158 |

4.2435 |

| 2 |

中债国债收益率曲线 |

2020-02-04 |

1.7475 |

1.7630 |

2.1000 |

2.4056 |

2.6399 |

2.7906 |

2.8551 |

3.4488 |

| 3 |

中债国债收益率曲线 |

2020-02-05 |

1.7475 |

1.7667 |

2.0773 |

2.4264 |

2.6348 |

2.7893 |

2.8440 |

3.4460 |

| 4 |

中债中短期票据收益率曲线(AAA) |

2020-02-05 |

2.7991 |

2.8975 |

2.9118 |

3.1949 |

3.4609 |

3.7157 |

3.9601 |

NaN |

说明:

ak.bond_china_yield() 是获取中国债券收益率曲线的接口。若你需要指定起始/结束日期,可查阅当前版本文档查看是否支持 start_date、end_date 参数。

代码中假设列名为 "期限(年)" 和 "收益率(%)",实际可能不同,请运行 print(df.columns) 检查并修改。

此处将”估算久期”简化为 到期期限 × 0.9,仅用于教学演示。若你有准确久期模型,可替换该假设。

绘图中采用双 Y 轴:左轴为收益率(蓝色)、右轴为估算久期(红色),帮助学生直观理解”到期期限 → 久期”及其与收益率关系。

模块 11. 风险分解与敏感度分析

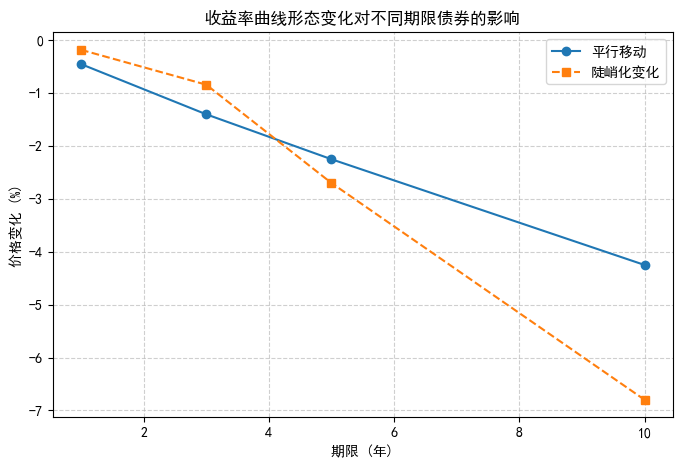

在组合管理中,久期只是利率风险的第一层。我们可以进一步分解风险来源: - 平行移动风险:整体收益率曲线平移; - 陡峭化风险:短端与长端利率变化不同步; - 曲率变化风险:中部利率变化导致曲率变化。

import pandas as pd

maturity = np.array([1, 3, 5, 10])

weights = np.array([0.3, 0.3, 0.2, 0.2])

duration = np.array([0.9, 2.8, 4.5, 8.5])

exposure = weights * duration

df = pd.DataFrame({'期限': maturity, '权重': weights, '久期': duration, '久期贡献': exposure})

display(df)

print(f'组合总久期 = {exposure.sum():.2f} 年')

# 模拟平行移动 vs 陡峭化

Δy_parallel = np.repeat(0.005, 4)

Δy_steep = np.array([0.002, 0.003, 0.006, 0.008])

ΔP_parallel = -duration * Δy_parallel

ΔP_steep = -duration * Δy_steep

plt.figure(figsize=(8,5))

plt.plot(maturity, ΔP_parallel*100, 'o-', label='平行移动')

plt.plot(maturity, ΔP_steep*100, 's--', label='陡峭化变化')

plt.title('收益率曲线形态变化对不同期限债券的影响')

plt.xlabel('期限 (年)')

plt.ylabel('价格变化 (%)')

plt.legend()

plt.grid(True, linestyle='--', alpha=0.6)

plt.show()

| 0 |

1 |

0.3 |

0.9 |

0.27 |

| 1 |

3 |

0.3 |

2.8 |

0.84 |

| 2 |

5 |

0.2 |

4.5 |

0.90 |

| 3 |

10 |

0.2 |

8.5 |

1.70 |

模块 12. 课堂练习与扩展案例

练习 1:久期匹配

给定: - 资产久期 5 年; - 负债久期 8 年; - 可投资短期债券久期 2 年、长期债券久期 10 年。 请计算各自投资权重以实现久期免疫。

练习 2:凸性调整

编写函数,计算债券价格变动的二阶近似: \[ ΔP/P = -D_{mod} Δy + 0.5C(Δy)^2 \] 并验证在不同 Δy 下,久期与凸性联合估计的误差大小。

练习 3:AkShare 拓展

使用 AkShare 调用 bond_zh_us_rate() 数据,比较中国与美国国债收益率曲线差异。